Our fund ranges include:

Tracker funds

Tracker funds are low-cost, institutional level portfolios designed to capture the global market return over the long term. Our robust and disciplined approach to investing is founded upon Nobel Prize-winning academic research and harnesses sophisticated tools to properly test investment solutions.

Environmental, Social and Governance (ESG) funds

Whereas traditional financial analysis considers only quantitative financial and economic data, environmental, social and governance investing attempts to incorporate other factors into the decision-making process.

The goal of our ESG portfolio range is to place greater emphasis on companies that are adhering to higher sustainability standards, while maintaining our low-cost, buy-and-hold, globally diversified approach that has been demonstrated to serve investors well over the long term.

ESG investments seek positive returns while also considering the impact business practices have on the environment and society.

Our ESG portfolios include a number of funds that have been subject to a thorough analysis of the underlying construction process, to ensure their ESG credentials. In addition, all of the funds fit our core investment philosophy, being good value, passively managed and maintaining a diversified market capital approach.

Factor funds

The key drivers of return are well documented in different global markets and across different time periods. They incorporate important findings from the work of the Nobel Memorial Prize in Economic Sciences winner, Gene Fama and his colleague, Ken French. Their research shows that, over the long term, smaller companies have higher expected returns than larger companies and value companies outperform growth companies.

So, factor funds are built to capture the premium offered by small and value companies.

It is important to note that this in no way suggests value and smaller companies will give excess returns every year, or that they are guaranteed. Indeed, value and smaller companies sometimes underperform for long periods relative to the overall market. However, academic evidence suggests that this is a price worth paying in the long term.

The evidence we use is the product of many decades of independent, peer-reviewed research and analysis by some of the world’s leading academics, including numerous Nobel laureates.

In other areas of life, medicine or law for example, decisions are routinely based on evidence, yet much of the investment industry ignores academic research. They rely instead on a blinkered belief that, armed with enough information, sophisticated software and the smartest minds, they can beat the market and be well paid for their efforts.

An evidence-based investor has science on their side, giving them peace of mind and over time, higher expected returns.

Unlike many investment solutions, Belmayne is not constrained by an allegiance to specific academics or product providers. We use only best-in-class funds, giving exposure to markets at the lowest possible price and improve our portfolios, as better suited or more cost-effective funds become available.

The fund management industry is constantly telling us we need to invest in actively managed funds to ‘beat the market’.

Unfortunately, evidence shows that, after costs, only a tiny proportion of fund managers succeed in beating their benchmark index in the long term (around 1%). Likewise, there is no reliable way to identify in advance the few actively-managed funds that are going to outperform. It takes 22 years of data to be 90% certain these managers are genuinely skilful, not just lucky.

Capital markets work

When capital and labour are put to efficient use, with the aim of generating the maximum wealth for those who take on the risk of enterprise, it is assumed free markets price financial assets effectively and fairly, based on supply and demand.

It is accepted that the UK and other developed nations, in which clients may invest, are broadly capitalist societies, where profits are ultimately expected to flow through to owners.

While this may not be the case for a small number of companies (the collapse of Enron, WorldCom, Lehman Brothers, Woolworths and Carillion left shareholders nursing large losses) or some emerging market economies, it is a fair description and expectation.

Risk and reward go hand in hand

A basic underlying assumption is that to achieve a higher level of return, an investor needs to assume a higher level of risk.

Don’t put your eggs in one basket

Diversification is a risk management technique that mixes a wide variety of investments, covering multiple asset classes and with no bias to a specific industry or segment.

The only certainty in financial markets is uncertainty, which requires an astute investor to take advantage of the diversification benefits available.

The portfolios we use are highly diversified across 23 developed and 24 emerging market countries, as well as more than 20,000 individual equities and bonds. This increases the opportunity to capture the benefits provided by capitalism around the world.

Download the full chart >>

Download the full chart >>We focus on minimising costs in the widest sense. We avoid the cost of underperformance by an active manager, use low-cost passive strategies, negotiate service provider discounts and manage investments in a tax aware manner, via the portfolio management service.

While investment costs might seem relatively small, they all add up. The power of compounding means you not only lose the amount you pay in fees, but also the growth that money might have made for years to come.

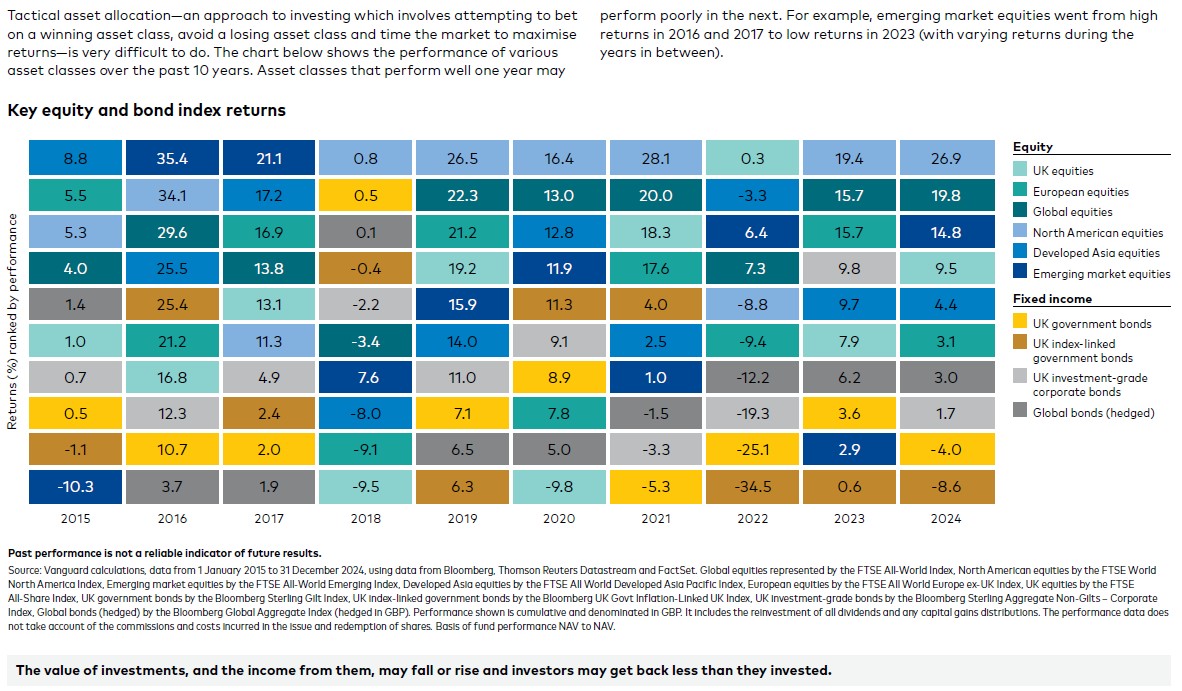

Numerous studies in the past 60 years have shown successful tactical asset allocation, otherwise known as market timing, is incredibly difficult.

In 1986, landmark research showed that asset allocation was the overwhelmingly dominant contributor (91.5%) to the total returns of an investment portfolio. Choosing the right stocks or mutual funds was not the main factor (4.6%), while market timing played an even smaller part (1.8%).

Trying to judge when a bear or bull market is about to start/end or when one asset class will perform better than another is futile. To repeatedly succeed at this, net of the costs incurred by buying and selling securities, is nigh on impossible. Investors, including the professionals, typically harm their returns by trading on these sorts of market calls. Research available on the S&P Indices Versus Active (SPIVA) website repeatedly demonstrates this year in, year out.

Many investment managers who claim to be passive, simply by virtue of the fact they use index funds, are in fact making active investment decisions. Typically, for example, their portfolios have a tactical asset allocation overlay. Regardless of whether you invest via index funds, active funds or individual shares, there is no reliable evidence that tactical asset allocation will deliver higher returns.

Based on this evidence, we employ a buy-and-hold policy, only trading to maintain strategic asset allocation within pre-set tolerance bands, or to replace funds with lower cost alternatives. From time to time, we may look to incorporate new funds to gain exposure to a new factor, but all in all, these activities lead to very little trading, reducing transaction costs and thus enhancing returns for investors.

Best-of-Breed

Our portfolios are built around ultra-low-cost index tracker funds that provide access to most of the world’s publicly available equities and bonds – the kind active fund managers have repeatedly been shown to struggle to beat.

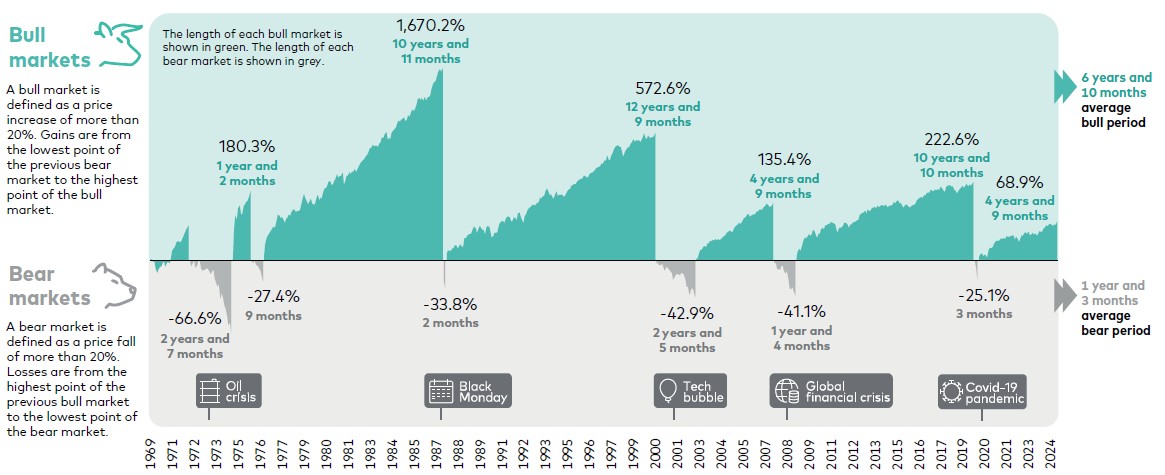

All too often, investors let their emotions get the better of them with dire consequences for returns. As financial planners, a key part of our role is to help you maintain a disciplined approach, especially in extreme market conditions.

Economic uncertainties, random market movements and the rise and fall of individual companies mean it is extremely difficult for anyone – including professional fund managers – to beat the market in the long term. There is a significant body of research to suggest that outperformance by most fund managers is down to luck rather than skill.

Download the full chart >>

Download the full chart >>Our investment portfolios are mapped to Belmayne’s risk profiling tool. In doing so, we can add clarity during risk discussions, to show why a portfolio would be appropriate. We then follow up with a discussion, using 94 years of data, to demonstrate worst case scenarios and help manage expectations at an early stage and at each review.